We are concerned with financial derivatives (derivative contracts) with value or price $V(S,t)$ and payoff which we generalize as $F(S)$. We assume the underlying stock price $S_t$ is driven by Brownian motion increment $dW_t = W_{t+dt} \; – \; W_t$. Our fundamental stock price model assumes that the return of the stock over the $t, t+dt$ interval is $$\dfrac{S_{t+dt} – S_t}{S_t} = \dfrac{dS_t}{S_t} = \mu dt + \sigma dW_t $$ $S_t$ then satisfies the stochastic differential equation (SDE) $$dS_t = \mu S_t dt + \sigma S_t dW_t \tag{1}$$ which is a shorthand notation for the stochastic integral equation[ref]Marek Musiela & Marek Rutkowski, Martingale Methods in Financial Modelling, Equation 3.2[/ref]$$S_t = S_0 + \int_0^t \mu S_u du + \int_0^t \sigma S_u dW_u, \quad \forall t \in [0, T^*]$$

- $\mu$ is the mean rate of return (time-1). This is a consequence of the 1976 paper by Ross which takes expectations of (1) conditional on information at $t$: $$\mathbb{E_p} \biggl[ \dfrac{dS_t}{S_t}\bigg{|} \mathcal{F}_t \biggr] = \mu + \sigma \times \underbrace{\mathbb{E_p} [dW_t]}_{0} = \mu$$

- $\sigma$ is the volatility (time-1/2)

- $W_t$ is a $\mathbb{P}$ Brownian motion

Given initial value $S_0$, the solution $S_t$ to equation $(1)$ above is a Geometric Brownian Motion with drift $\mu$ and variance $\sigma^2$:

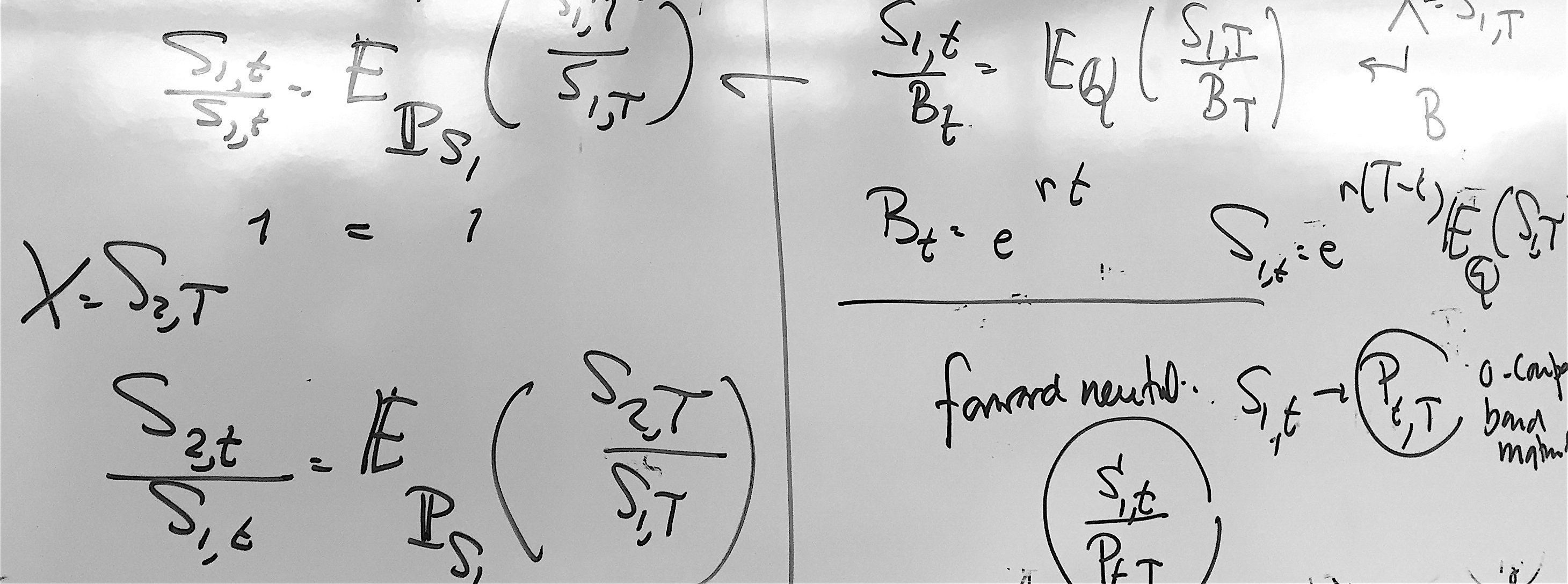

Risk-neutral stock price dynamics

The Arbitrage Theory of Capital Asset Pricing – Stephen A. Ross states that the return $\mu$ must be composed of the risk-free rate plus one risk premium. It is a special case of the CAPM (see below). $$\mu = r + a = r + \sigma \lambda \quad, \quad \lambda \in \mathbb{R}^n$$

where $\lambda$ is the market price of equity risk. Substituting this in $(1)$ adds a drift to the Brownian motion and “destroys” it. \begin{align*}

dS_t &= (r + \sigma \lambda) S_t dt + \sigma S_t dW_t\\

& = r S_t dt + \sigma S_t (\underbrace{\lambda dt + dW_t}_{d\widehat W_t})

\end{align*}$\mathbb{E_p} [d\widehat{W}_t] \neq 0$. But clearly $$\mathbb{E_p}[d\widehat{W}_t] = \mathbb{E_p} [\lambda dt] + \mathbb{E_p} [dW_t] = \mathbb{E_p}[\lambda dt ] + 0$$ However, thanks to Girsanov’s theorem, we can now construct a new process under risk neutral measure $\mathbb{Q}$ equivalent to $\mathbb{P}$ \begin{align*}

dS_t &= r S_t dt + \sigma S_t d\widehat{W}_t \tag{3}

\end{align*} such that $\widehat{W}_t$ is a $\mathbb{Q}$-Brownian motion. Hence$$\mathbb{E_Q} [\widehat{W}]= 0 \quad, \quad \mathbb{E_Q} [d\widehat{W}]= 0 $$ Further details of the Girsanov Theorem here.

Arbitrage Theory of Capital Asset Pricing is a special case of the CAPM, with ONE risk factor $F_1$ $$r_f + b_{j} \Bigl(\mathbb{E_p} \Bigl[ \tilde \delta \Bigr] – r_f \Bigr)$$ whereas the for the CAPM we sum $q$ risk premia, each one a fraction of the excess risk premium for each one of $q$ risk factors. $$r_f + \sum_{i=1}^q b_{ji} \Bigl(\mathbb{E_p} \Bigl[ \tilde \delta_i \Bigr] – r_f \Bigr)$$

Black-Scholes PDE (Hedging Portfolio)

Constitute a portfolio $\Pi_t$ of one unit of a derivative $V(S,t)$ and an amount $\partial_s V (S_t, t)$ of stock sold short. $$\Pi_t = V (S_t, t) \; – \; \Delta_t S_t$$ At $t + dt$ , the change in value of $V (S_t, t)$ is given by Itô’s lemma for $f(X_t, t)$.

$$dV_t = (\partial_t V + \frac{1}{2}\sigma^2 S^2_t \partial^2_sV)dt + \partial_sV dS_t$$ The change in the $\Delta_t S_t$ short stock is simply $\Delta_t dS_t$. The portfolio gain(or loss) is the net change resulting from the change in derivative and short stock over $dt$ and by definition this change is risk free. Hence $$d\Pi_t = \underbrace{(\partial_t V + \frac{1}{2}\sigma^2 S^2_t \partial^2_sV)dt}_{\text{known at }t} \; + \; \underbrace{\partial_sV dS_t \; – \; \Delta_t dS_t}_{\text{risky component}}$$

We choose the short stock delta $$\Delta_t = \partial_sV$$ This is actually the definition of the delta, the change (with respect to the stock $S$) of the derivative $V(S,t)$. Because the portfolio change is risk free, the risky term must equal zero. This leaves $$d\Pi_t = (\partial_t V + \frac{1}{2}\sigma^2 S^2_t \partial^2_sV)dt$$ Now, the same gain can be realised by investing $\Pi_t$ in a savings account over the time frame $t$ to $t + dt$. By the absence of arbitrage principle, these two gains are equal. $$(\partial_t V + \frac{1}{2}\sigma^2 S^2_t \partial^2_sV) = r \Pi_t dt$$ Substituting our original expression for $\Pi_t$ we then obtain that $V(S,t)$ satisfies the partial differential equation

\begin{align}& \dfrac{\partial V}{\partial t} + \dfrac{1}{2}\sigma^2 S^2 \dfrac{\partial^2 V}{\partial S^2} + r S \dfrac{\partial V}{\partial S} – rV = 0 \quad (t < T)\\

\\& V(S,T) = F(S)\end{align}This is the ubiquitous Black-Scholes partial differential equation. The payoff at expiry function $F(S)$ gives the appropriate boundary condition for $V$ when $t = T$. We may also express the equation as[ref]Manuel Ammann, Credit Risk Valuation. Eqn 2.12[/ref] as

$$V^t + \dfrac{1}{2}\sigma^2 S^2 V^{SS} + rSV^S – rV = 0$$ and derived either by applying Itô’s lemma to a hedging argument, by a truncated Taylor’s expansion of the log of the GBM above or via the CAPM. The Black and Scholes equation has an infinite number of solutions. A particular solution is associated with a particular derivative by virtue of the derivative’s payoff at expiry $F(S)$ which gives the appropriate boundary condition for the PDE. We can then solve the Black Scholes

- by transforming the PDE into an initial value problem for the heat equation

- by probability theory known as the Feynman Kac method

Assumptions of the Black-Scholes Model

- There exist two instruments traded in continuous time with no restrictions as to quantity or sign of position:

- one risky asset $S$ (e.g. a stock),

- one riskless asset $M$ growing at the short-term rate $r(t)$ (e.g. a money-market account).

- The economy has the following simplifying properties:

(a) no transaction cost on $S$ or $M$ (relaxed in 1987 by Leland and later in 1995 by Avallaneda)

(b) no dividend payment on $S$ (relaxed by Merton in 1973)

(c) in the original paper, ”interest rates are constant.” In actuality, only short-term interest

Computations

European Call

European Put

Put Call Parity

The Greeks